Ep597: Lance Depew – You’re Going to Lose Despite Your Best Efforts

Listen on

Apple | Google | Spotify | YouTube | Other

Quick take

BIO: Lance Depew has over 30 years of equity research, portfolio management, and corporate finance experience.

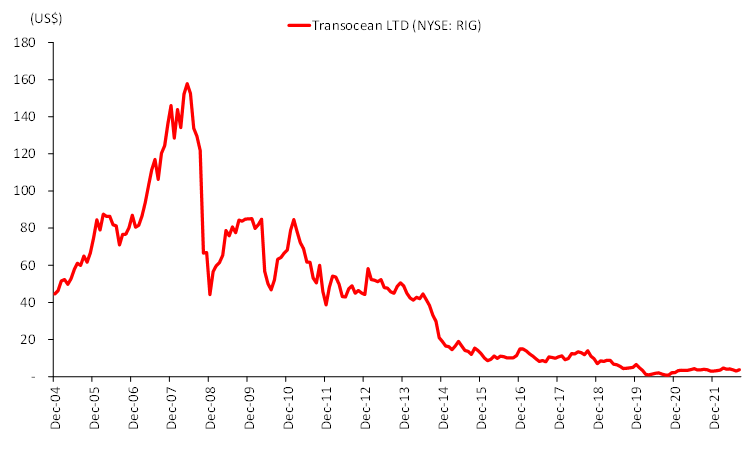

STORY: Lance’s worst investment was in a company called Transocean. He bought shares on in 2006 at $80.35 a share. He ultimately exited the position in 2020, when the shares sold at less than $1 a share.

LEARNING: Regardless of how smart you are and how much homework you do, things can go wrong when investing. Take steps to de-risk your positions.

“Despite your best-laid plans, things can still go wrong.”

Lance Depew

Guest profile

Lance Depew has over 30 years of equity research, portfolio management, and corporate finance experience.

Since 2000, he has co-managed Railay Capital Partners, L.P., a global multi-strategy absolute return hedge fund.

Between 1994 and 2007, Lance was a portfolio manager and director of equity research for Leading Assets United Ltd., the premier asset management firm dedicated to both public and private equity investments in the Thai market.

Mr. Depew received his MBA in finance at the Anderson Graduate School of Management at UCLA and is currently a member of the investment committee for the Santa Barbara Museum of Natural History.

Worst investment ever

Lance’s worst investment was in a company called Transocean. On January 30th, 2006, Lance’s fund management company bought the shares at $80.35 each. They ultimately exited the position on October 7th, 2020. The last sale took place at less than $1 a share.

At the time Lance was investing, Transocean had about a billion dollars of net debt, which was pretty modest relative to its market cap, which was below the $20 billion range. It wasn’t a highly leveraged company, nor was it trading at a high multiple. The utilization rates for the various assets in the industry were also very high. Further, Transocean was the number one company in terms of dividends paid to investors. The company looked like it would be an excellent investment with all these factors.

Unfortunately, several things went wrong, leading to a steep share price fall. The first problem was the global financial crisis.

The second problem was the 2010 deepwater explosion in the Gulf of Mexico. This crisis weighed on transactions and significantly impacted the stock price.

The third problem occurred in March 2020 when the Saudi Arabia and Russia oil price war kicked in as the two countries were duking it out in the global commodity markets. This war tanked the oil price for some time.

The fourth problem was the global pandemic. There was complete and sudden demand destruction that ultimately led to the price of oil dropping into negative territory for a brief period.

Lessons learned

- Regardless of how smart you are and how much homework you do, things can and will go wrong when investing.

- Don’t let one lousy investment weigh on your psyche. Just continue to plug away. Over time, you’ll be rewarded if you invest wisely.

- Invest in value, and you’ll get positive returns on investment.

- Investments can turn sour despite attempts to understand a company and an industry entirely. So you just got to anticipate that there are going to be unforeseen events during your investment journey.

- Occasionally, resort to timely sales as a way of de-risking your positions and bringing back some return on your investment.

Andrew’s takeaways

- You’ll lose despite your best efforts as a fund manager, so have a risk management plan in place.

- Take steps to de-risk your positions.

- Try and get different opinions on what you’re trying to invest in.

Actionable advice

Read as much as possible—especially financial journals such as the Wall Street Journal. Do as much research as possible and learn as much as you can about companies and industries, macroeconomic conditions, global events, etc. This will help you when it comes to putting your portfolio together.

No.1 goal for the next 12 months

Lance’s number one goal for the next 12 months is not to lose money and to earn positive rates of return on investment.

Parting words

“Thank you very much for your time, Andrew. I wish everyone the best of luck this coming year.”

Lance Depew

Andrew Stotz 00:02

Hello, fellow risk takers and welcome to My Worst Investment Ever, stories of loss to keep you winning. In our community, we know that to win in investing, you must take risk but to win big, you got to reduce it. Ladies and gentlemen, I'm on a mission to help 1 million people reduce risk in their lives and that mission has led me to create to Become a Better Investor Community. In that community, you get access to our global asset allocation strategies and stock portfolios, our investment research, weekly live sessions and the risk reduction lessons I've learned from more than 500 guests go to my worst investment ever.com to claim your spot now. Fellow risk takers this is your worst podcast host Andrew Stotz from a Stotz Academy, and I'm here with featured guests. Lance Depew. Lance, are you ready to join the mission?

Lance Depew 00:52

Yes, I am. Yes, I am.

Andrew Stotz 00:54

Yes, and you too. I'm looking forward to this chat. And let me introduce you to the audience. Lance has over 30 years of equity research portfolio management and corporate finance experience. Since 2000, he has co manage Riley Capital Partners, a global multi strategy absolute return hedge fund between 1994 and 2007. Lance was a portfolio manager and director of equity research for leading assets united, the premier asset management firm dedicated to both public and private equity investments in the Thailand market. Lance received his MBA in finance at the Anderson Graduate School of Management at UCLA and is currently a member of the Investment Committee for the Santa Barbara Museum of Natural History. Lance, take a minute and tell us about the unique value that you bring to this world.

Lance Depew 01:49

Well, I don't know if I bring unique value I, I've been in the industry for a long time, well over 30 years, and I actually wanted to start off. And my goal initially was to be a jazz musician, like my father. But I realized early on that I didn't have enough talent to really, you know, make it to really be successful as musician. So I transitioned ultimately, to finance and economics I really early on, found that I had a love for, for finance and economics. And it led me down this path. And I've been Portfolio Manager, again for over 30 years. So I love it. It gets me I'm always interested, always learning. And it's never it's never a dull moment. Never a dull moment.

Andrew Stotz 02:40

I remember, we met originally in Thailand many years ago when you were living here. And I always, you know, saw you as a very thoughtful analyst, fund manager investor. And I wonder for a young person listening to, you know, to this and thinking about, you know, for me, I talk a lot about a sell side analyst, you know, what's the career like? And what's that like, but for you, I kind of consider you a biocide, portfolio analyst or portfolio manager, but you're also a pretty strong analyst, maybe you could just give an idea of like, why you liked that career? What what is that career bring to you?

Lance Depew 03:18

Well, when you're on the buy side, you're it's really your own intellectual pure curiosity. And in the effort you put into analyzing companies, it's not I don't want to be rude towards people on the sell side. But, you know, it's not a kind of a used car salesman ship type of role where you're trying to pitch ideas and stocks and generate commissions, you know, running a hedge fund, it's, it's all about performance, right? At the end of the day, if you don't lose less than the market, if you don't generate returns and absolute in an absolute sense, you're not going to get paid. So you have to take that insight and the hard work and it has to be translated into real gains. And, you know, that's the only time you get to share in the spoils is when you when you actually generate real returns for your investors. So we're there's an alignment of interests, which you don't quite get on the on the sell side. Definitely. So I prefer being on the buy side. And I've actually never been on the sell side. But I love being on the buy side. I wouldn't, I wouldn't want to any other career.

Andrew Stotz 04:22

And how would you describe you know, your you taught your strategy is global, multi-strategy, absolute return? What is what are those three things mean to someone who doesn't know much about, you know, investing?

Lance Depew 04:38

Well, a lot of time a lot of funds are focused on a particular market. So you're going to be a US growth manager or a biotech manager concentrated in the US or a single country fund in Japan or China or Thailand for that matter. So we do truly invest globally. Our portfolio currently doesn't have a huge allocation to non-US equities, which has actually been a good thing given the outperformance of the US market and the US dollar in recent years. But so again, we do invest. And we do look at opportunities globally. We are value investors. So we're not we're definitely not growth managers, we're not technical analysts, we are looking for undervalued opportunities in the market. And we don't shy away from small-cap opportunities, big cap or large, you know, it doesn't do the whole range. We're not pigeonholing ourselves into any one category of stock or industry, or, or in from a geographic standpoint, we're looking at every, you know, all opportunities. Yep. But as far as an absolute return, sorry, an absolute return says what we try to do. And I like to know if I coined the phrase, but we like to look at things in theirs fixed income, we like to look at fixed equity. So I like to create more structured returns on our underlying equity investments. And most of the time, that's done through options. So you know, a lot of your investors or your listeners are familiar with covered call strategy. So a lot of our underlying long positions are coupled with calls with long with short call options. And that creates more of a structured return environment, it can, it can obviously, Cap some of your upside, potential, but it also reduces your downside risk. And so we like to create equity returns that I, I guess what I'm what ultimately we're getting at is, I would prefer a stable, you know, 10% return than a very volatile 12% return. And I think a lot of our investors feel that way as well. So we do that through the structured equity investments that we make.

Andrew Stotz 06:55

So let's make it simple for a lute listener who doesn't understand that type of stuff. The first thing is you identify a stock that you like, and you've done your research, and you think this is going to do better than the market, I think it is going to do really well over the next senator three years, let's say. And so a typical long only investor would say, I'm just going to buy that and hope that everything goes and when it collapses by 20, or 30%, I'm going to buy more, and when it collapses by 40%, I'm going to buy more. But there's a risk, you know, at some times they come back from that fall, other times they don't. So I believe when you talk about your strategy, what you're saying is that you're using an option to truncate the downside to say, Okay, I'm only going to I'm not going to capture all of that downside, I'm going to give up a little bit of the upside, but I'm going to protect myself on the downside is that is that describe what you're doing?

Lance Depew 07:51

Yeah, more or less, I mean, there are different ways to do this. And so we have many different approaches, and depends on the stock. And a lot of there's a lot of dynamics involved. But let's just take a simple example, let's just say we feel the stock is, is fairly to undervalued at $80 a share and we buy a share, you know, buy a, you know, hundreds of shares of $80, we might write the 100 strike calls of that company, let's say we get $5 a premium. If, in that very simple scenario, we bought the shares at 80, the shares can move up to $100. And we participate in all those gains. If the stock pays dividends, we receive any and all dividends. But if the shares move above 100, we are capped at the $100 value. But remember, we received the $5 of income by selling this call by giving up part of that, that upside. So in the event that the shares do drop, let's say they'd dropped from from $80 to 75, we've essentially still are at a breakeven level because we receive the $5 from writing the call. So it's that sort of approach where we're we're giving up some of the upside potential, but it creates some downside protection that we wouldn't otherwise have. And so when you take into account dividends, you can write calls with different maturities, different strike prices, we oftentimes don't write calls against our entire position that way, let's say if the shares double or triple, we're still participating in some portion of those gains. So it's how we structure these investments. With these options, calls and puts in such a manner it creates more of this tailored return that our investors or our are hopefully you know they expect from us.

Andrew Stotz 09:44

And would I be correct in saying if we think about a crude way of handling a price for a trader? They may say okay, I bought it at 80 If it goes to 70 I'm out. Now long only funds Andrew generally doesn't do that. And therefore, you don't want to have some sort of instrument, or stop loss that's getting you out of the stock, what you're trying to do is cushion the blow by saying, Okay, if it goes down to 70, I've already gone down 10, but we got the five in income. And therefore we've cushion the blow of the fall is that that describe what you're doing?

Lance Depew 10:22

Exactly. Now, we may decide to buy more shares at that lower price level, we may buy back the call option and write a new call option at 90 or 85. Because the shares have gone down, we profit on the first call, and we write a new call. It's limiting our upside to a greater degree. But it's still it's generating income. And to the extent that we can de risk our our investments over time, it just increases our ability to risk to to earn positive returns on investment, that's really what our investors are looking for. They want us to earn absolute returns on our investment, we want to protect against the downside. And we want to generate positive returns. And our investors aren't looking to you know, shoot or like in a take a baseball analogy, you got baseball players that are shooting for the fences, we're more like we try to be the rock crew. And maybe this will go over the head of number of your listeners. But you know, Rod Carew is known for just hitting singles and doubles and just had a high batting average. And that's what we're trying to always do always get on days don't have to, you know, hit a homerun, we just want to get on base, we don't want to strike out, we don't have to homerun but we want to get on base

Andrew Stotz 11:29

on it. And one other thing I know that you, you are interested in both large companies and small companies, companies in America companies outside doesn't matter what the size of the company or where you're buying the company to as whether you can get access to these type of hedging strategies, or is it pretty much available for every, every every stock everywhere?

Lance Depew 11:56

It's actually it is actually difficult to do that unless you're a large enough fund, it's it's not always possible to right option contracts in other countries. So all of our option trading does take place in the US. But there are a number of foreign companies that are actively traded in the US. So you can write options against certain foreign companies. But again, we are we are global and we are multi strategy. And we're value investors. So if it's a Norwegian company that we feel is undervalued, we'll buy those shares. And if there's no options, there's no options. And we'll monitor it as a separate investment. And through dividends or other means we'll we'll be looking to protect and to, you know, see a decent return on investment over time. So it has to really, it has to make sense and options help things make sense. But all times we are just purely naked long. It's not always coupled with options.

Andrew Stotz 12:53

Got it? Well, I mean, I think this is why I'm happy to have you on the show, because you've gotten a lot of experience in this area. And I believe you are going to share some stories about stocks. So now it's time to share your worst investment ever. And since no one goes into their worst investment thinking it will be. Tell us a bit about the circumstances leading up to and then tell us your story.

Lance Depew 13:13

Well, I'd say I was thinking long and hard about this because obviously, as an investor, it's been in the business for many, many years. I do want to point out that my very first investment, the very first day I invested was I bought a few 100 shares of Bank of America. And it was the Black Monday in I think it was in October of 1987. That was my very first purchase of any company on the stock market. Because I saw on the news like the stock market is cratering. And so I went out and I called my broker and it's like, I don't even know if I had a broker at the time, but somehow I was able to call someone and I was able to put I was a young kid, I placed my order for two or 300 shares and I think the shares were trading at eight or $9 a share and I still own their shares to this day but it was that was my first investment. But as far as my worst investment I'm not sure if it is actually the worst but it's among the worst would probably be my investment in a company called Trans ocean. ticker symbol is ri G rig. We invest in both personally but in my fund. We first established a position in rig on January 30 of 2006. So it was quite a quite a while ago. And I was looking back at our records and the purchase was made at $80.35 A share that was our very first investment. Now we ultimately exited the position our fully exited the position on October 7 of 2020. And we the last sale took place at less than $1 a share so doesn't take a genius to realize that was not a good investment. Now, I will say that a long The way we sold shares at higher levels than the $1, we received dividends. During a portion of the that that holding period, the company was flush with cash for a period of time. And we did right call options, which many of those call options ended up expiring worthless. And then we wrote new call options. But we didn't, we weren't able to write enough call options fast enough to guard from the, you know, the the almost, you know, 100% discretion of value. Transition is still around, it's still a very viable company. It's the largest company, offshore drilling company in the world. It's probably the most recognized and sophisticated fleet. So it is clearly the leader in the sector. But the sector has really gone through some very, very tough times. And unfortunately, you know, our investors suffered through many of those tough times. So maybe I should just point out a few particulars. At the time, our investment rig had about a billion dollars of net debt, which was fairly modest, modest relative to its market cap was in the low $20 billion range. So wasn't a highly leveraged company. It was trading at a relatively modest four forward, Evie to EBIT multiple. And I don't know if that if that's a multiple that your listeners are familiar with. But it's basically taking the enterprise value of a company which has its market value, plus the the value of its debt, less its cash, that's the enterprise value, and dividing that by the kind of operating cash flow or one measure of cash flow that companies generate. And so it was not trading at a very high multiple. And against this backdrop, backdrop, excuse me, the industry was the utilization rates for the various assets in the industry was very, very high at the time. So the contract durations were long day rates were high, companies were just throwing up massive amounts of cash. There were a lot it was a very fragmented industry, there were many players. The fleet was quite old. There had been very few. Very few assets had been scrapped. When we first were moving into this into the investment.

Andrew Stotz 17:30

One thing I would add, I think the backdrop to is that if it's 2006, you are getting into it, oil prices rising high. And so environment was fantastic. Oh, yeah, it

Lance Depew 17:43

was a great, you know, again, not a lot of debt, comfortable, multiple of earnings. And the industry dynamics looks strong. This was the number one company starting to pay dividends, it took a while before dividends came in, they bought another competitor GSF. And, you know, it just looked like this would be a great investment going forward. So what happened, what went wrong? Well, a number of things went wrong. The first problem was the global financial crisis. So just give you just to put things in perspective, in June of 2008, oil was at $140 a barrel. By February of oh nine, it had dropped to $39 a barrel. So that led to companies like you know, it hurt the entire first of all, the globe, like suffered a major dislocation. But you know, oil companies suffered, and rig went from a high of $163. So there was a point in time where we actually had a gain on our, we had a good, decent return on investment, but it dropped to the low 40s by early 2009. So I think that was really due to it wasn't it was more against this macro economic backdrop, as opposed to looking at, you know, something that the company did wrong or something within the industry, per se, nothing really changed within the industry. And that's one of the reasons why we stayed in the investment. We didn't say, Oh, my goodness, you know, the fundamentals have changed. Yes, oil prices have dropped, we've had the, you know, SNL crisis and, you know, property crisis and all these things that have taken place in the US, but the fundamentals for the offshore drilling space still prepared sound as far as we were concerned. And again, as I mentioned earlier, the fleet itself was quite old and there was a need for scrapping to take place. So we felt that a number of the older assets would have would be scrapped. Now, during this time, when there were when the companies in the sector were doing quite well and were flush with cash, they did go on a new building spree. And so the the new build Orderbook did start to grow during this timeframe. And I was hopeful as I believe many investors were at the time that you'd have this transition, many of the older rigs would be scrapped. And the newer ones would come in seeing when that's they see a massive increase in the overall size of the offshore drilling fleet.

Andrew Stotz 20:18

So to summarize where things are at this point, like, basically, okay, we got in at 80. But you know, things came down. Now we're at 40. It's understandable, oil prices have absolutely collapsed, this company has survived and collapsed. And if somebody was coming to this company right now, and they can buy it at 40, it's gonna be a great deal. I think that's so okay. So things seem to be, you know, it was a big macro hit.

Lance Depew 20:48

But, yeah, let you know, we're value investors. And we felt that, you know, even though the stock had suffered it, you know, we were hopeful and believe that the outlook was good. So it was the second problem. The second problem was the 2010 deepwater explosion in the Gulf of Mexico, and that was a trans ocean rig. So that really upset the applecart. And really, not only did it hurt the entire industry, but it really in particular, really weighed on transactions, so that I didn't put down the the impact that had on the stock price. But I mean, it clearly had a very significant impact on that price. I just didn't note it for your listeners. But that had a huge impact. And that was really, again, it's a one off, and there's nothing you could have done to anticipate that sort of event, right? Or the ramifications of that. And it wasn't just the event, it's what impact it had on the entire industry, and how people how politicians viewed offshore drilling and the risks, the environmental risks. And so that really just it again, it took the stock down, and the valuation down another, you know, another chunk down, and from where it had been, even though we're starting to recover from the global financial crisis, and then boom, this hit again. So you know, it was another body blow?

Andrew Stotz 22:11

And can I ask a question about that? Because I think, you know, as an outsider, whether you're an analyst, a fund manager, an analyst at a fund management company, you only have so much information. Now, it's possible that an insider may be predicting that something could go wrong, or could have seen that, okay, we're slipping on our safety, or whatever, that you know what that was, but as an outsider, I think there are you have to accept the fact that there are limits to what we can really know about what's going in, going on inside that company. How do you see that just so that, you know, I be curious, your thoughts there?

Lance Depew 22:49

Well, transaction has had a fantastic safety track record. They were they are they were in continue to be the leading company in the offshore drilling space, they have the most sophisticated assets. And the thing is, when you look at in the case of the Deepwater Horizon, the the operator, when they talk when they refer to the operators, they're actually the oil companies. And it was British Petroleum that was operating the rig. So they were actually even though the rig was owned by trans ocean, and it was their crew, the operator was British Petroleum. So British Petroleum, ultimately, faced the most significant liability, like 80, or 90%, of the total cost of that oil spill was borne by British Petroleum, because they were the ones operating the rig, they were directing transition in certain respects, their personnel what to do, and what steps they were going to take, as far as you know, their drilling and the production that they were things that they were doing at the time, that it was really directed by British Petroleum. So that's why they were the ones that were more that faced the highest liability. But other than that, and again, it was very misfortunate. It was It was tragic. And it was but again, it was very much a one off tragic event, you know, and those things do happen. And you have that's why we have portfolios, right. That's why we don't have 100% of our investment in any one stock. But it's a sort of thing you can't I believe you can't anticipate. So there's a few other prompts that that that took place the third and I believe I have the dates correct. But in March of 2020 you have the Saudi Arabia, Russian oil price war that kicked in when Saudi Arabia and Russia were duking it out in, in the global commodity markets as far as you know, who is going to control the price of oil and that really tanked the oil price for a period of time. And when you look at offshore drilling and the oil majors, you know, their ability to invest in the future. You know it you know, they are long, long lead times and, and a lot of these deepwater oil fields take, you know, 10s of billions of dollars to develop. So it's a it's a long term investment proposition. But when you've got this kind of oil price war taking place or other math, macroeconomic headwinds, when those events take place, it shakes the confidence and it might delay some of these very significant investments that oil majors are looking at. And so again, that weighs on utilization rates, day rates, and, you know, ultimately, the share price of a company like trans ocean, because, you know, the oil majors are backing up and saying, Wait, you know, maybe we're not going to, you know, tie up this rig for, for two years at, you know, $450,000 a day, let's, let's, let's, let's wait for six months and see how things shake out. So that was a third problem. And ultimately, the fourth problem was the global pandemic. And, as we all know, I'm sure your listeners know, you had such a complete and sudden demand destruction, it ultimately led to the price of oil dropping into for a brief period of time into negative territory, I mean, literally, oil prices were negative. So, you know, oil majors, were not looking to be drilling offshore, in the, you know, deepwater Gulf of Mexico or offshore Brazil or other places in the world, because, you know, it just didn't make sense. And, you know, the world was on hold. So those were the four main kind of abrupt shocks to the system that really weighed on transaction and investor sentiment in the stock. And just also, I think it's important to point out that we also had the shale revolution that was kind of taking place throughout this timeframe, it was like more of a slow revolution, but it was a very significant one. And I've seen studies that show that had it not been for the shale revolution, that oil prices would have potentially been up to 36%. Higher than then they were the you know, because of the shale revolution, it kind of brought you know, because of the success that the US EMP companies had, particularly in like the Permian Basin in Texas, and now New Mexico, that that huge increase in oil output on shore, you know, a lot of oil majors were like, say, well, maybe we don't need to, like start doing as much EMP activity in these deepwater regions, where it is ultimately more expensive, we can just go and tap into the shale, you know, take advantage of the shale and the fracking. And that's where we're going to get a better return on investment. So

Andrew Stotz 27:50

I would say that, I thought my memory serves me correct. It's probably about the time that Trump came into office that that revolution was kind of hitting its peak production.

Lance Depew 28:01

Yeah, it had been going on for a number of years, but it really hit its peak. And but then with, with that, Saudi Arabia, Russian price war, a lot of those wells were shut in and with the Biden administration, you know, in the pandemic, it really led to a very significant drop in in output, as well, as you know, the number of rigs that were drilling on shore dropped tremendously. So the total output of production in the US domestically onshore, dropped quite significantly. And that's one of the things that you can do in the in the shale, the fracking and shale plays, you can turn on and off these, these rigs a lot more readily, more readily than you can, let's say, the oil sands in Canada or the offshore deepwater fields. So those are meant to be on just kind of continuously,

Andrew Stotz 28:56

right. I want to go through this just because you've laid it out very clearly. Let's just say the share price starts at $80, let's say roughly, and GFC hits the global financial crisis that brings it down by about from 80 to about 40. Roughly, then, then in 2010, Deepwater Horizon, what was the share price kind of roughly after that?

Lance Depew 29:25

I have to look here in 2010. So if the stock went back up into the low 80s, yep, maybe upwards of 80 or 90, yep. And then with the deep water, it went from that $80 range, and then it dropped back down to like 20 or $30.

Andrew Stotz 29:46

Okay, so then it was at 20 or 30. And then it managed to survive the deep water and then we have the shale revolution. I'm going to call that point two to A. So the shale revolution Brought the share price down further or flat or

Lance Depew 30:03

so yeah, there was a recovery, the stock dropped immediately after the Deepwater Horizon, then it went back up. And then it's been on this,

Andrew Stotz 30:13

where was it after deep water when it recovered from deepwater, roughly.

Lance Depew 30:18

So I'm looking at here, so back around January of 2011, it was back around $80. Okay. And then from that point, it pretty much continued along and steady slide down. And again, Against this backdrop, you have to look at the the the structure of the industry, you have a lot of these older, second generation third generation fourth, fifth, you know, the sixth generation, the the the floaters, and you have the jackups, you have all these different fleets you have, you had a very large, very legacy fleet that was very old and hard to maintain. But a lot of those rigs, the owners were looking to deploy those to get them contracted, because otherwise they're either warm stack or cold stack. And it's it, there's a cost involved in warm stacking your rig, there's a, there's a more significance cost in cold stalking a rig, and to get those rigs back in, in production. Also, there's a cost involved to do that as well. So a lot of these industry players were holding out hope that if they just were able to withstand a little more pain, eventually they could get these rigs back in service, and started generating return on investment.

Andrew Stotz 31:33

So what but what I'm trying to understand now is what was the what was the final nail in the coffin that caused the slide down, you know, to $1 or less or whatever?

Lance Depew 31:46

Well, it's been this, this, it's been many years for this hope for recovery to take place that hasn't, even to this day, clearly taken hold. So every step along the way, when market watchers investors like ourselves, we're anticipating that, okay, we've seen the bottom, and now things are going to turn, there's either been a huge macro shock, or it's just been this long, steady. You know, malaise that's taken place where the players, the utilization rates have remained depressed. So as long as you see utilization rates of the rigs, if there's a large number of rigs available, warm, stacked or cold stack, it's very difficult to see rates, day rates increasing until you start seeing utilization rates pop up to, you know, that more like 80 to 90% range. So until you see that, you know, with in, you've got, you know, there's debt obligations. And so these companies are not like debt free. So they're, they're, they're losing money, they're not generating positive returns on investment. So it's kind of a, it's just tiny Chinese water, torture, so to speak. And it's taken a number of years, but it's just wait on the company and on the sector. We've had a number of bankruptcies we've had in the cup, the industry has consolidated. And some companies have reemerged from bankruptcy. They're their debts have been restructured. And so you've got new credit creditors that are now shareholders. And all of this has had an impact, particularly on the transition because transition never went through that formal restructuring the way like a Seadrill and others did, they get a clean sheet, they don't have the debt overhang. But they still have the rigs and so the rigs are waiting and trying to get employed. And the operators are seeing like, hey, we don't have to pay the foreigner and $50,000 a day that we want to pay, we can pay 300,000 Well, if you're paying 300,000, given the costs, you know, the capital that you've got investment, three and $1,000 is better than zero, but it's not generating, you're not generating positive economic returns on investment that you that you need to see a stock price, not only, you know, staying, you know, seeing a stock price increase in value, it's not going to happen until you get higher rates of return. And you won't get those higher rates until you see utilization rates improve.

Andrew Stotz 34:08

So I just pulled up the share price. And I can see why it's a little bit difficult to kind of nail down what you know, but I I'm gonna include this share price, a picture of the share price in the show notes. So for those people interested in kind of watching the chronology, we'll have that in the show notes. I think it's it's good now to walk into the part of this podcast where we ask, what did you learn?

Lance Depew 34:31

Okay, well, I would say that, that, you know, investments can turn sour, despite any and all attempts to fully understand a company and an industry. So you just got to realize that, you know, I hate to you know, cuss but you know, shit happens. It really does. So, it just you, you have to anticipate that there are going to be unforeseen events. So just despite your best, you know, best laid plans that still things can go wrong. So you have to take that into account when you are in vesting. And that's why, you know, one of the main reasons why investors should always have a portfolio. I think another important lesson is that hubris is, is probably your worst enemy. And a lot of investors, you know, investors are smart people, you know, a lot of these hedge fund guys, and then all these other people. They're really, really smart. But I think oftentimes, that can be to their detriment, because if you think you've got all the answers, and you know more than anyone else, that you're not going to, you know, listen to different views, you're not going to, to make your investments in such a manner that, that, you know, you anticipate that you might be getting things wrong, or that these other, you know, events outside your control, like the Deepwater Horizon can actually take place. So you have to anticipate, and realize that you really don't have all the answers. So that's the second thing. And I'd say finally, you always should take steps to de risk your positions. So as I mentioned earlier, you know, we we sell options, constantly using options to generate income and to de risk our positions. You also should, on occasion, resort to timely sales. I'm not saying trade in and out of positions, but on occasion, you might want to take some capital off the table. And then dividends, dividends are always something that you don't want to you know, they're not unimportant. And so it's a way of de risking your positions and bringing back some return on your investment. So those are probably the my three lessons that I learned, at least from this transaction investment.

Andrew Stotz 36:49

So let me I want to go into that a little bit. Just because I think there's a lot there's a really good lesson. So you've talked that should happens in gotta be diversified, just foundational risk management, you've got to have in place. Number two is hubris, hubris, or just, you know, the confidence that comes with being an analyst, you know, and analyzing, you know, you naturally are trying to find stories that you can build confidence. And as we went through this story, it kind of flashed me back where I remember some encounters with you, and maybe some emails or something where I came across your, your, your confidence in the industry, you know, in, in drilling, and in, you know, that whole industry. And it just kind of reminded me of that, and that that gets me to the question I have is that. So the question I have is, what could you do that, what could you have done differently? I mean, you did a lot of things, right, there was a lot of different environmental things that just hit global financial crisis, Deepwater Horizon, you know, that type of stuff. But what, what is one or two things that you think back and think, yeah, I should have at this point done that.

Lance Depew 38:05

I wish I had the answer. I really don't know. Because I'd like to second guess and think back, you know, what would I have done that different, but I really don't, you know, unfortunately, I think I probably would have done the same thing, if the same sort of, you know, circumstances were to present itself. Again, I wish that, you know, that weren't the case. But I think that, you know, I still think transmission, you know, is poised at some point to recover. Now, that night, it's trading in the $3 range, though, maybe it goes to nine or $10, you know, so from here, as a new investor, you might get a decent return on investment, but looking at it now. So just to point out this stock again. Now, the other thing that does concern me now that it's does have a pretty significant amount of of net debt relative to its market value. So there's still there is now relative to when I first invested, there's a lot more financial risk in the stock than there was when we first invested. But, you know, maybe we should have just cut our losses earlier, and redeployed our capital at an earlier point in time. Unfortunately, I didn't do it to the detriment of our investors.

Andrew Stotz 39:21

So let me let me summarize some of the takeaways, I mean, I think that is a great summary of what you said shit happens, you know, overconfidence and, and also the lesson of de risking your position. I think what I want to highlight is is your answer to the last question, and that is, I'm not really sure. I think I did most things right. And I probably would do it the same way. And I wrote down when you said that, for the listeners out there who want to be a fund manager or investor. Bad news, you're going to lose. You are going to lose despite your best efforts. Absolutely. And I think that this is really a lesson in that. And if you understand that right from the beginning, first it makes, then you make sure that you have a risk management in place. So that's the first thing, I think many people will go in thinking, I'm not gonna, I mean, I'm doing all the work, I'm doing a lot of effort here, I've got a lot of good information, but sorry, you're gonna lose. And I think that's kind of my number one takeaway. I think, at the end of this podcast, I always end by saying, you know, by listening to these stories, it helps us to create, grow and protect our wealth, I always say that we create wealth through either our job, maybe you get a good salary, and you don't spend as much of it and you can invest every single month, that's like creating wealth every single month, or you got a business and you're generating cash flow, that's another way of creating wealth, growing wealth we do in the stock market, generally, you know, or in other people's businesses, let's say, or in government bonds, you know, some people are just gonna say, I'm gonna grow my wealth in a very slow way. And then the third one is protect our wealth. And that's what this podcast is all about. And I think that, I just want to highlight that, you know, there's core principles in place for anybody who's building a portfolio, and that is, particularly the diversification. The second thing that you've talked about is, how can we de risk this portfolio? And, you know, it's given me some some thoughts about the, you know, what I'm managing here and thinking about it. And so, and then the last thing I put down, and this is kind of a wimpy, final point, and that is get different opinions. But I think that it's really hard to do. Like what, who would have come to you with a informed opinion on the topic, and have convinced you that it's time to get out of this? I just don't see that that would have been the case. But, you know, we try to get opposing views. But when you think you've done the research, part of what makes this fund manager successful is to say, No, I'm against the opposing view. So that's how I would summarize what I've learned is anything you would add to that?

Lance Depew 42:11

Well, I do have a partner, and we debated transition many times over the years. And, you know, looking back, he was clearly right, you know, he was against, you know, the position as it soured, you know, didn't think it was going to recover. And I kept pushing that, you know, I think it you know, it will, and these are all the reasons why I think it stands to recover, or, you know, it just was down because of the spill, or because of the macro, this or the macro of that. And so, you know, I had my arguments, and he had his arguments. And, you know, there were times when we reduced the position, but, you know, ultimately, within our last sales, we're at a fraction of the initial, you know, stock price that when we first moved in, in 2006. So it was a rather painful episode. And, you know, in, in a fun that, again, overall, we've made, you know, quite good returns on investment, our investors have generated close to 9%. Returns, even going back to March of 2000, we first started the fund. So on average, we've generated very steady positive returns on investment. So yes, we had, you know, in transition is not the only investment that's gone bad, but you have to, you have to have conviction, you have to do your research. But regardless of how smart you are, and how much homework you do, things can go wrong, have a portfolio de risk. And, and don't let one bad investment weigh on your, you know, on your psyche, you know, you're always going to have those kinds of investments and just continue to plug away. And I think over time, you will be rewarded every investor, if you invest wisely. Invest in value, you take some of these steps that I've outlined, I think you'll you'll be looking at positive returns on investment.

Andrew Stotz 44:02

It makes me think about my first 10 years in Thailand, I was riding motorcycles a lot. And I had different motorcycles and proposition that's a very risky proposition. And, and when I sold my motorcycles and got out of that, that game, I somebody asked me, you know, whenever I see anybody buying a motorcycle, they, you know, I taught them I just say, look, it's not a question of, if it's a question of when you're going to have an accident. It is not a question of it, particularly for those people listening and viewing who know Bangkok traffic. And so, you know, it's the same thing with investing, you know, it's not a question of, you know, oh, if if you're going to lose, you are going to lose, and you've got to be prepared for that. So based on what you learn from this story, and what you continue to learn. Let's go back in time, let's imagine a young person now facing a similar situation. What one action would you recommend our listeners take to avoid suffering the same Fate?

Lance Depew 45:02

Well, you had actually asked me earlier about what lessons or what advice I would give investors. So maybe they turn your question around a little bit. One thing that's really helped me over the years and I remember distinctly, I don't know the exact date, I do recall those in 1985. I, I subscribed to The Wall Street Journal, and I have literally, from that day forward, I have never, I've read every single issue cover to cover from that day to 1985 Till today, and if I'm on a vacation for a week or two, I'll have a stack of Wall Street Journal's. And I'll sit for hours and I'll go through all the stories in you know, some of its, you know, personal finance and, you know, movies, this and that. But there's politics, there's macroeconomics, and there's, there's, there's a lot of information about businesses. And I think it's a really, really useful tool. And, and, and I highly recommend that investors read as much as possible. And the Wall Street Journal is a great source, it could be the Financial Times, it could be other publications, but I think doing as much research as possible, learning as much as you can about companies and industries, macroeconomic conditions, global events, it'll really, really help you when it comes to putting together your own investments in your own portfolio.

Andrew Stotz 46:25

Well, that's the first time we've had that recommendation, I think it's a great one. And for the listeners out there, you know, find that

Lance Depew 46:32

over 600 visits and or fixed six 600 calls, how not one person on person

Andrew Stotz 46:38

is recommended that Nope, you're the first and I think that the lesson for the listeners is that, you know, find your reliable source of good financial information, whether that's the ft or I also really enjoy the economists and some of the articles, you know, particularly there's summaries of research and stuff, and Wall Street Journal also, but find that source and dedicate yourself to learning on a daily basis. And I think that if you do that, that's super valuable. So

Lance Depew 47:08

we have Bloomberg, but Bloomberg is, you know, it's not something that most your, your listeners can afford to pay unless they're in the industry. So I wouldn't, you know, that's not something I could really recommend.

Andrew Stotz 47:19

Last question, what what is your number one goal for the next 12 months

Lance Depew 47:25

to preserve the capital in our fund. So, again, most important thing is not lose money for our investors, we are actually down this year, we are outperforming the s&p as a whole. But our goal is to to not lose money, and to earn positive rates of return on investment. I don't know if we'll be able to do that this year. But that's our goal. Preserve the wealth of our investors, we are stewards. And you know, that's our number one priority is to protect the capital that people have, have, you know, they've given us the opportunity, it's quite a distinction to have people, you know, give, you know, their their net worth, like your, you know, please help us manage this for our retirement because we invest in our own assets, my partner and I, a significant portion of our net worth is tied up in our funds. So we gain and lose money along with our other limited partners. And I've,

Andrew Stotz 48:17

I've seen and received your email for many years. And, you know, despite, you know, mistakes or frustrations like translation as an example, your performance has been excellent. And it's also a very steady performance, which is not the same as you know, a lot of others. So I think, is there a place that is a website or someplace that I can send people that are interested that want to look at it more

Lance Depew 48:42

with, you can always direct people to me by email, but we don't, unfortunately, we're pretty small. And we don't have all the bells and whistles and the marketing team and all that other stuff that goes along with most large hedge funds. We're pretty small by design. Keep it simple, but we're more than happy to talk to people.

Andrew Stotz 49:01

So if anybody's if anybody's interested, because Lance is also another interesting guy, and that he doesn't have all these social media places and all these different ways of contacting. So if you want to learn more, just let me know and I'll put you in touch. Well, listeners, there you have it another story of loss to keep you winning. If you haven't yet joined the Become a Better Investor Community. Just go to MyWorstInvestmentEver.com right now to claim your spot. As we conclude, Lance, I want to thank you again for joining our mission. And on behalf of A. Stotz Academy I hereby award you alumni status for turning your worst investment ever into your best teaching moment. Do you have any parting words for the audience?

Lance Depew 49:45

No, but thank you very much for your time Andrew and I wish everyone Best of luck this coming year.

Andrew Stotz 49:53

Fantastic. Fantastic. And ladies and gentlemen, that was a masterclass in understanding about investing. to the upside the downside, how to understand risk and the reality that shit does happen. And that's a wrap on another great story to help us create, grow and protect our well fellow risk takers. Let's celebrate that today. We added one more person, Lance to our mission to help 1 million people reduce risk in their lives. This is your worst podcast host Andrew Stotz saying I'll see you on the upside.

Connect with Lance Depew

Andrew’s books

- How to Start Building Your Wealth Investing in the Stock Market

- My Worst Investment Ever

- 9 Valuation Mistakes and How to Avoid Them

- Transform Your Business with Dr.Deming’s 14 Points

Andrew’s online programs

- Valuation Master Class

- The Become a Better Investor Community

- How to Start Building Your Wealth Investing in the Stock Market

- Finance Made Ridiculously Simple

- Best Business Book Club

- Become a Great Presenter and Increase Your Influence

- Transform Your Business with Dr. Deming’s 14 Points

Connect with Andrew Stotz:

About the show & host, Andrew Stotz

Welcome to My Worst Investment Ever podcast hosted by Your Worst Podcast Host, Andrew Stotz, where you will hear stories of loss to keep you winning. In our community, we know that to win in investing you must take the risk, but to win big, you’ve got to reduce it.

Your Worst Podcast Host, Andrew Stotz, Ph.D., CFA, is also the CEO of A. Stotz Investment Research and A. Stotz Academy, which helps people create, grow, measure, and protect their wealth.